No matter how big or small your business or organization is in Dallas, or even how long it has been established, you have worked hard to build it into what it is today. You have worked tirelessly, perhaps even using your own money and time to bring it to fruition — why leave it unprotected?

The main purpose of business insurance is to protect your business from expected costs as well as unexpected potential financial losses that can occur due to a natural disaster, an accident on the premises, a lawsuit, or other expensive incident. Unexpected costs such as these can blindside your business debilitating, and even completely obliterating your operation, if you don’t have the provisions that business insurance offers. Though business insurance is an additional operating cost, it can save you money in the long run and may even save your business if a costly event should occur.

The type of insurance that you need is ultimately dependent on the type of business that you have. Some businesses will need more coverage due to the nature of their operations, and some will require less. However, most businesses need coverage that can be broken down into four categories:

The best way to make sure you have the right coverage is to talk to one of our business insurance experts. We have partnered with a variety of business types in the area and are familiar with the risks that those operations pose for the business. Learn more on the Powell Insurance Group website and contact us to get a free quote.

Whether you are a seasoned business person or you quit your day job and launched your dream business, you need business insurance. Like any type of insurance, having it can not only offer you peace of mind in the present by knowing you’re covered, but you can also help you rest assured that when the worst happens, you will be protected financially.

When you are running a business, there is a lot that has to go right for it to be successful.This also means there is a lot that could go wrong; there are many threats that could hurt, deabilitate, or completely ruin your business. However, when it comes to what business insurance can offer, it’s not just about the unexpected costs, but also those that are easily foreseeable as you run your business.

Here are the possible costs that business insurance can cover:

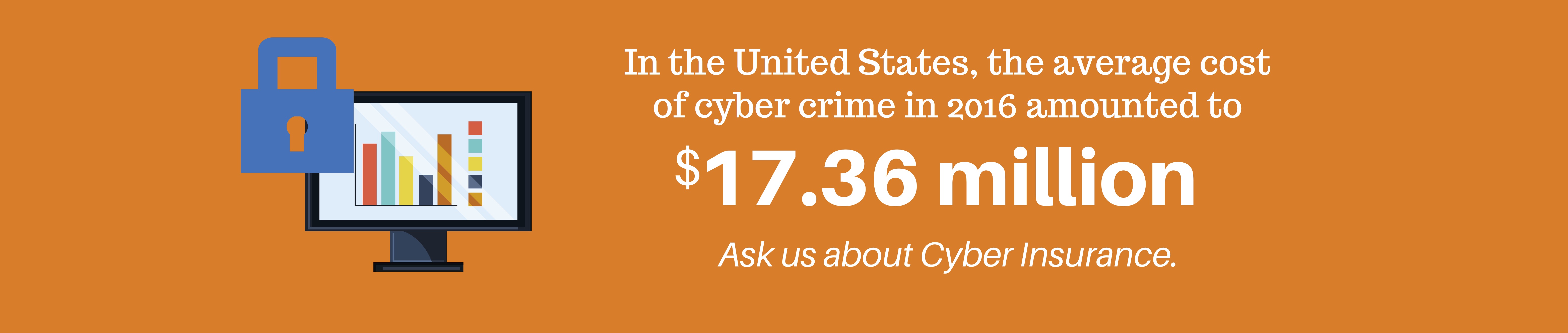

Cyber-insurance is an insurance product used to protect businesses and individual users from Internet-based risks, and more generally from risks relating to information technology infrastructure and activities. Risks of this nature are typically excluded from traditional commercial general liability policies or at least are not specifically defined in traditional insurance products. Coverage provided by cyber-insurance policies may include first-party coverage against losses such as data destruction, extortion, theft, hacking, and denial of service attacks; liability coverage indemnifying companies for losses to others caused, for example, by errors and omissions, failure to safeguard data, or defamation; and other benefits including regular security-audit, post-incident public relations and investigative expenses, and criminal reward funds.

Insurance companies selling business insurance offer policies that combine protection from all major property and liability risks in one package. (They also sell coverages separately.) One package purchased by small and mid-sized businesses is the businessowners policy (BOP). Package policies are created for businesses that generally face the same kind and degree of risk. Larger companies might purchase a commercial package policy or customize their policies to meet the special risks they face.

BOPs include:

1. Property insurance for buildings and contents owned by the company — there are two different forms, standard and special, which provides more comprehensive coverage.

2. Business interruption insurance, which covers the loss of income resulting from a fire or other catastrophe that disrupts the operation of the business. It can also include the extra expense of operating out of a temporary location.

3. Liability protection, which covers your company’s legal responsibility for the harm it may cause to others. This harm is a result of things that you and your employees do or fail to do in your business operations that may cause bodily injury or property damage due to defective products, faulty installations and errors in services provided.

BOPs do NOT cover professional liability, auto insurance, worker’s compensation or health and disability insurance. You’ll need separate insurance policies to cover professional services, vehicles and your employees.

Professionals that operate their own businesses need professional liability insurance in addition to an in-home business or businessowners policy. This protects them against financial losses from lawsuits filed against them by their clients.

Professionals are expected to have extensive technical knowledge or training in their particular area of expertise. They are also expected to perform the services for which they were hired, according to the standards of conduct in their profession. If they fail to use the degree of skill expected of them, they can be held responsible in a court of law for any harm they cause to another person or business. When liability is limited to acts of negligence, professional liability insurance may be called “errors and omissions“ liability.

Professional liability insurance is a specialty coverage. Professional liability coverage is not provided under homeowners endorsements, in-home business policies or businessowners policies (BOPs).

As a businessowner, you need the same kinds of insurance coverages for the car you use in your business as you do for a car used for personal travel — liability, collision and comprehensive, medical payments (known as personal injury protection in some states) and coverage for uninsured motorists. In fact, many business people use the same vehicle for both business and pleasure. If the vehicle is owned by the business, make sure the name of the business appears on the policy as the “principal insured“ rather than your name. This will avoid possible confusion in the event that you need to file a claim or a claim is filed against you.

Whether you need to buy a business auto insurance policy will depend on the kind of driving you do. A good insurance agent will ask you many details about how you use vehicles in your business, who will be driving them and whether employees, if you have them, are likely to be driving their own cars for your business.

While the major coverages are the same, a business auto policy differs from a personal auto policy in many technical respects. Ask your insurance agent to explain all the differences and options.

If you have a personal umbrella liability policy, there’s generally an exclusion for business-related liability. Make sure you have sufficient auto liability coverage.

Business interruption insurance can be as vital to your survival as a business as fire insurance. Most people would never consider opening a business without buying insurance to cover damage due to fire and windstorms. But too many small businessowners fail to think about how they would manage if a fire or other disaster damaged their business premises so that they were temporarily unusable. Business interruption coverage is not sold separately. It is added to a property insurance policy or included in a package policy.

A business that has to close down completely while the premises are being repaired may lose out to competitors. A quick resumption of business after a disaster is essential.

1. Business interruption insurance compensates you for lost income if your company has to vacate the premises due to disaster-related damage that is covered under your property insurance policy, such as a fire. Business interruption insurance covers the profits you would have earned, based on your financial records, had the disaster not occurred. The policy also covers operating expenses, like electricity, that continue even though business activities have come to a temporary halt.

2. Make sure the policy limits are sufficient to cover your company for more than a few days. After a major disaster, it can take more time than many people anticipate to get the business back on track. There is generally a 48-hour waiting period before business interruption coverage kicks in.

3. The price of the policy is related to the risk of a fire or other disaster damaging your premises. All other things being equal, the price would probably be higher for a restaurant than a real estate agency, for example, because of the greater risk of fire. Also, a real estate agency can more easily operate out of another location.

If you’re running a business from your home, you may not have enough insurance to protect your business equipment. A typical homeowners policy provides only $2,500 coverage for business equipment, which is usually not enough to cover all of your business property. You may also need coverage for liability and lost income. Insurance companies differ considerably in the types of business operations they will cover under the various options they offer. So it’s wise to shop around for coverage options as well as price.

Regardless of the type of policy you choose, if you’re a professional working out of your home, you probably need professional liability insurance. Some types of in-home businesses, such as those that make or sell food products or sell home-made personal care products, may have to buy special policies.

To insure your business, you have three basic choices, depending on the nature of your business and the insurance company you buy it from.

They are:

Homeowners Policy Endorsement.

You may be able to add a simple endorsement to your existing homeowners policy to double your standard coverage for business equipment such as computers. For as little as $25 you can raise the policy limits from $2,500 to $5,000. Some insurance companies will allow you to increase your coverage up to $10,000 in increments of $2,500.

You can also buy a homeowners liability endorsement. You need liability coverage in case clients or delivery people get hurt on your premises. They may trip and fall down your front steps, for example, and sue you for failure to keep the steps in a safe condition.

The homeowners liability endorsement is typically available only to businesses that have few business-related visitors, such as writers. But some insurers will provide this kind of endorsement to piano teachers, for example, depending on the number of students. These endorsements are available in most states.

In-Home Business Policy/Program.

An in-home business policy provides more comprehensive coverage for business equipment and liability than a homeowners policy endorsement. These policies, which may also be called in-home business endorsements, vary significantly depending on the insurer.

In addition to protection for your business property, most policies reimburse you for the loss of important papers and records, accounts receivable and off-site business property. Some will pay for the income you lose (business interruption) in the event your home is so badly damaged by a fire or other disaster that it can’t be used for a while. They’ll also pay for the extra expense of operating out of a temporary location.

Some in-home business policies allow a certain number of full-time employees, generally up to three. In-home business policies generally include broader liability insurance for higher amounts of coverage. They may offer protection against lawsuits for injuries caused by the products or services you offer, for example.

In-home business policies are available from homeowners insurance companies and specialty insurers that sell stand-alone in-home business policies. This means that you don’t have to purchase your homeowners insurance from them.

Businessowners Policy (BOP).

Created specifically for small-to-mid-size businesses, this policy is an excellent solution if your home-based business operates in more than one location. A BOP, like the in-home business policy, covers business property and equipment, loss of income, extra expense and liability. However, these coverages are on a much broader scale than the in-home business policy.

A BOP doesn’t include workers compensation, health or disability insurance. If you have employees, you’ll need separate policies for these coverages.